Crypto Payments vs Bank Transfers: What Is Actually Different?

Crypto payments vs bank transfers compared: settlement time, fees, reversibility, cross-border cost, and access requirements. What the architectural difference means in practice.

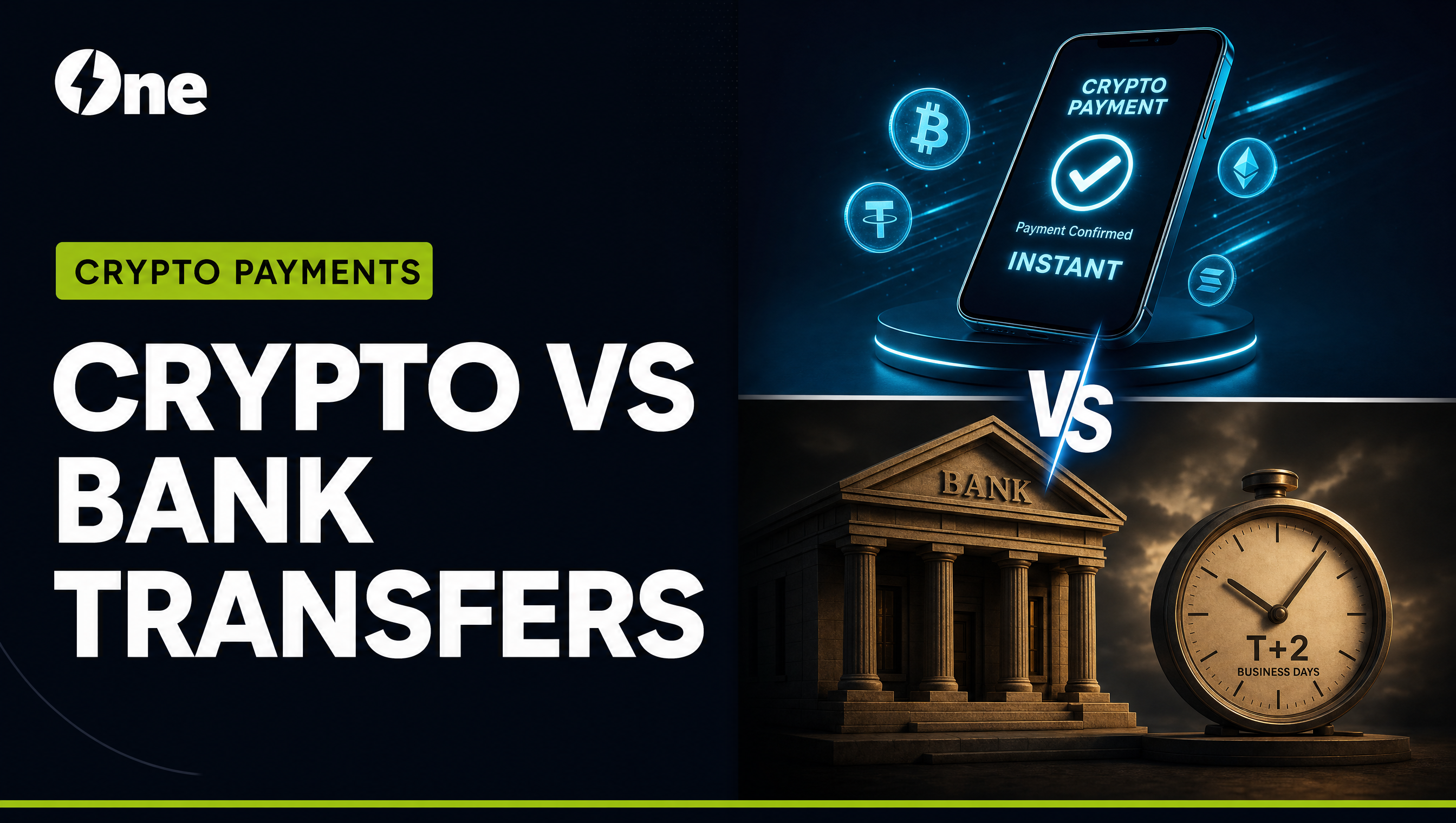

A SWIFT international wire costs $25–$50 and takes one to five business days. A USDC transfer on Base costs $0.002 and takes two seconds. That difference is not primarily about speed or price. It is about architecture.

A bank transfer moves a number in a database controlled by a private institution. A crypto payment updates a ledger distributed across thousands of nodes with no single point of control. Every practical difference between the two, including settlement time, reversibility, cross-border cost, and access requirements, flows from this single architectural distinction.

What to Know

- Bank transfers move value through a chain of private institutional ledgers; crypto payments update a shared distributed ledger directly.

- Bank transfers settle in 1–5 business days depending on method; stablecoin payments on modern chains settle in seconds.

- Bank transfers can be reversed through institutional authority; confirmed crypto transactions cannot.

- International bank transfers carry $25–$50 in fees plus FX conversion costs; stablecoin transfers cost fractions of a cent.

- Bank accounts require identity verification and institutional approval; a crypto wallet requires only a private key.

- Neither is universally better. The right choice depends on counterparty, value, use case, and regulatory context.

The Architectural Difference

When you initiate a bank wire, you instruct your bank to debit your account and credit another institution's account. Your bank sends a message through SWIFT (or a domestic equivalent like Fedwire or CHAPS), which routes the message to the recipient bank. Each bank updates its own internal ledger, so correspondent banks in between may hold funds temporarily during routing. The process is sequential, involves human-operated institutions, and depends on each participant following through.

When you initiate a USDC transfer, you broadcast a signed transaction directly to the Base network. Thousands of validators independently verify the transaction and update the same shared ledger simultaneously. There are no correspondent nodes, and no institution can freeze the transaction mid-flight. No party can fail to "follow through" because no party is trusted to act. The protocol enforces the transfer.

This is the structural difference. Everything else is a consequence of it.

Side-by-Side Comparison

| Property | Domestic ACH | SWIFT Wire | Credit Card | USDC on Base | Bitcoin |

|---|---|---|---|---|---|

| Settlement time | 1–3 business days | 1–5 business days | 1–2 business days | ~2 seconds | 10–60 minutes |

| Reversibility | Up to 60 days | Recall during clearing | Up to 120 days | None after confirmation | None after confirmation |

| Cross-border fee | N/A (domestic only) | $25–$50 + FX spread | 1.5–3% FX conversion | Under $0.01 | Variable, no FX |

| Access requirements | Bank account + KYC | Bank account + correspondent | Merchant account + card network approval | Wallet address only | Wallet address only |

| Minimum viable amount | Typically $1+ | Often $100+ (fees make small wires uneconomical) | Usually $0.50+ | No practical minimum | No practical minimum |

| Transaction transparency | Private (visible only to institutions) | Private | Private | Public on-chain | Public on-chain |

When Bank Transfers Are Still the Better Option

Despite crypto's structural advantages, bank transfers remain the right choice in several contexts.

Counterparty requires it. Most governments, large enterprises, and regulated entities still require bank transfers for payments. Payroll, supplier payments, and tax remittances typically must flow through the banking system.

Regulatory compliance is clearer. Bank transfers have well-established AML and KYC frameworks that compliance teams understand. Crypto compliance frameworks are still developing in many jurisdictions, and some regulated industries cannot accept crypto payments under current licensing conditions.

Reversibility is a feature, not a bug. Businesses that routinely process refunds, disputed transactions, or test payments may prefer a system where errors can be corrected. The irreversibility of crypto cuts both ways.

Consumer preference. Most retail consumers are not yet equipped to pay in crypto. Forcing a crypto-only checkout on general consumers will cost you conversion rate.

When Crypto Is Clearly Better

There are specific scenarios where the architectural advantage of crypto is decisive.

Cross-border B2B payments. Paying a supplier in Southeast Asia, a developer in Eastern Europe, or a freelancer in Latin America via SWIFT costs $25–$50 per transaction, takes days, and sometimes requires the recipient to have a correspondent banking relationship their local bank may not maintain. Stablecoins on modern chains eliminate all three friction points.

High-risk or high-chargeback merchant categories. Businesses in industries where card networks impose excessive chargeback thresholds, high reserves, or outright bans, including certain digital goods categories, iGaming, and global subscription services, find crypto the only reliable payment option at scale. There are no chargebacks on confirmed crypto transactions, and there are no card network approval requirements.

Global digital products. SaaS companies selling to customers in 50 countries, each with different card acceptance rates and FX costs, can offer a single stablecoin checkout that works identically everywhere. One integration, one fee structure, and no per-country payment method complexity.

Micropayments. A card payment under $1.00 is economically impossible at standard interchange rates. A USDC transfer of $0.05 is practical on Base or Solana, which means pay-per-use, pay-per-call, and metered billing models become commercially viable.

The Hybrid Approach Most Serious Businesses Use

Most businesses adding crypto payments do not replace their existing payment stack. They add crypto as an additional rail alongside card and bank transfer options. This gives customers choice without forcing adoption.

The practical architecture is to maintain card processing for consumer-facing retail, maintain ACH or wire infrastructure for institutional and domestic B2B payments, and add crypto rails for cross-border payments, high-risk categories, digital goods, and customers who prefer to pay in stablecoins or crypto.

A single crypto payment API that handles multiple chains and tokens, rather than managing per-chain integrations, makes this addition operationally tractable. AIO provides a unified API for multi-chain stablecoin and crypto pay-ins, with a 0.3% fee structure and no payout fees, designed for businesses running this hybrid model. The integration adds a new payment rail without replacing your existing stack.

For a detailed look at how crypto payments settle on-chain, see How Do Crypto Payments Actually Work? For the international payments angle specifically, see Stablecoin Payments vs SWIFT.

Frequently Asked Questions

Are crypto payments faster than bank transfers?

For most cross-border payments, yes, significantly. A USDC transfer on Base settles in roughly two seconds. An international SWIFT wire takes one to five business days. Crypto's speed advantage is most pronounced for international payments where correspondent bank chains add days and fees.

Can a crypto payment be reversed like a bank transfer?

No. Confirmed crypto transactions are irreversible. There is no payment network authority that can reverse them. Bank transfers can be recalled during the clearing window, and card payments can be disputed for up to 120 days. For merchants, crypto's irreversibility eliminates chargeback fraud but also means mistakes cannot be corrected through the payment network.

Do I need a bank account to accept crypto payments?

No. Crypto payments are received directly into a wallet address you control. You do not need a bank account, a payment processor relationship, or a merchant services agreement. This is particularly significant for businesses in markets with limited banking infrastructure, or for high-risk merchant categories that struggle to maintain card processing relationships.

What is the cheapest way to send money internationally?

Stablecoins on low-fee networks like Base, Solana, or Polygon are currently the cheapest documented method for international value transfer, with transaction fees under $0.01 and no FX conversion loss. SWIFT wires cost $25–$50 in fees plus a typical FX spread of 1–3%. Remittance services vary widely but rarely match stablecoin economics at scale.

Frequently Asked Questions

Are crypto payments faster than bank transfers?

For most cross-border payments, yes — significantly. A USDC transfer on Base settles in roughly two seconds. An international SWIFT wire takes one to five business days. Domestic ACH in the US takes one to three business days, though same-day ACH is available for some transaction types. Crypto's speed advantage is most pronounced for international payments where correspondent bank chains add days and fees.

Can a crypto payment be reversed like a bank transfer?

No. Confirmed crypto transactions are irreversible — there is no payment network authority that can reverse them. Bank transfers can be recalled during the clearing window, and card payments can be disputed for up to 120 days. For merchants, crypto's irreversibility eliminates chargeback fraud but also means mistakes — wrong address, wrong amount — cannot be corrected through the payment network.

Do I need a bank account to accept crypto payments?

No. Crypto payments are received directly into a wallet address you control. You do not need a bank account, a payment processor relationship, or a merchant services agreement. This is particularly significant for businesses in markets with limited banking infrastructure, or for high-risk merchant categories that struggle to maintain card processing relationships.

What is the cheapest way to send money internationally?

Stablecoins on low-fee networks like Base, Solana, or Polygon are currently the cheapest documented method for international value transfer, with transaction fees under $0.01 and no FX conversion loss. SWIFT wires cost $25–$50 in fees plus a typical FX spread of 1–3%. Remittance services vary widely but rarely match stablecoin economics at scale.